Release: June 4th at 1.30pm GMT+1

Reading time: 9 minutes

Two comprehensive surveys are used to provide economists and investors a snapshot of the employment situation in the United States each month, through the Household Survey and Establishment Survey—often referred to as the Payroll Survey. Both surveys provide a complete picture of the Labour market.

- The Household Survey derives data from approximately 60,000 households, led by the Bureau of Census for the Bureau of Labour Statistics, or BLS. The survey includes farm, non-farm, self-employed (unincorporated) and domestic helpers.

- The Establishment Survey tends to capture the spotlight. Through what’s known as the Current Employment Statistics (CES), each month the program gets in touch with approximately 144,000 businesses—representing nearly 700,000 worksites—targeting the payroll of non-farm businesses, non-profit groups and government organisations across the United States.

Due to its timeliness, accuracy, and importance within the broader economy, the employment situation report is a closely monitored indicator.

In most cases, the non-farm payrolls report (taken from the establishment survey) attracts the majority of attention, often vibrating through financial markets. A favourable number (generally considered USD positive) reveals additional jobs were added to the economy, while a negative value (often viewed as USD negative), displayed as -100k or -90k, for example, means jobs were lost in non-farm business.

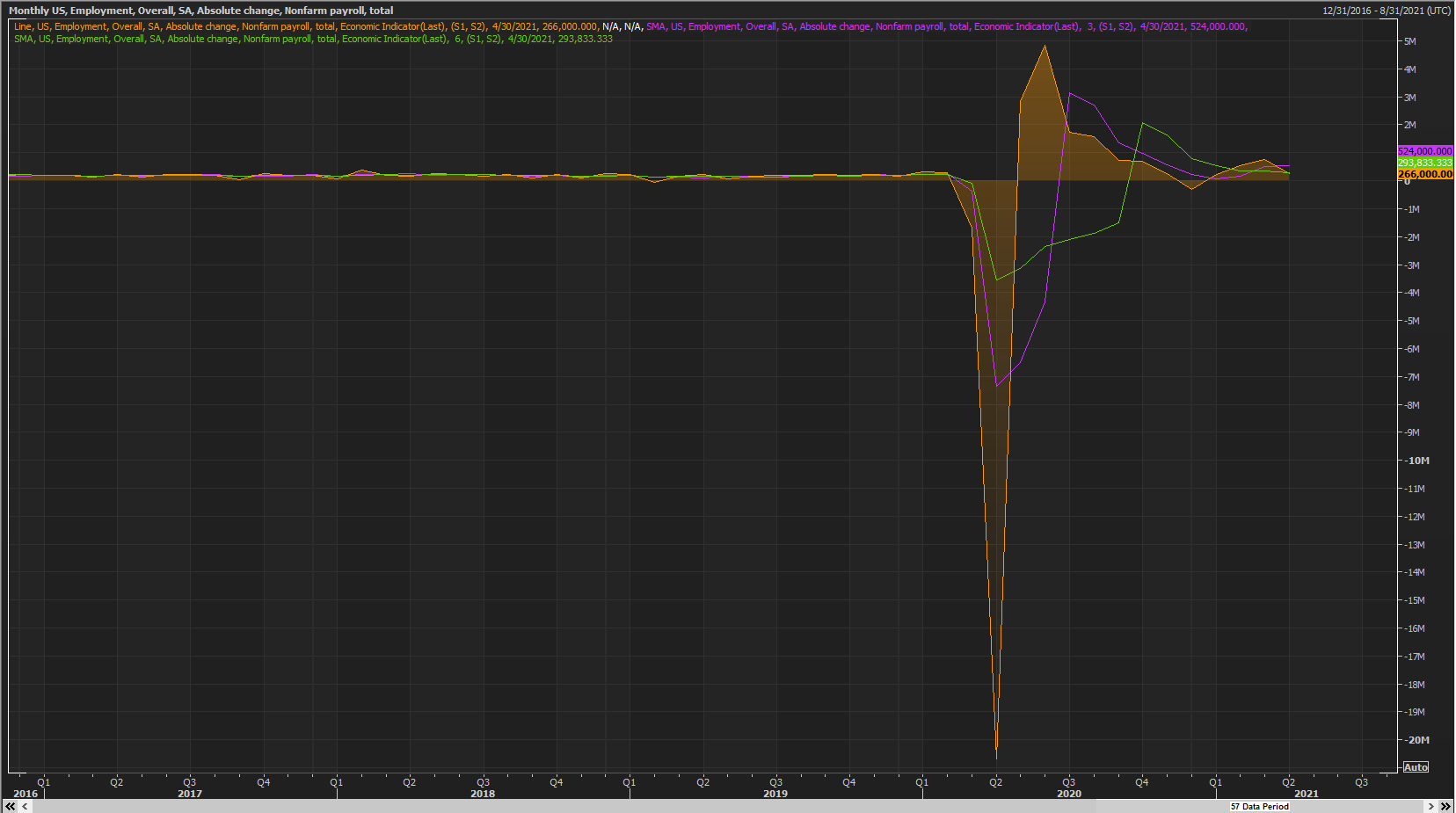

April’s non-farm payroll’s release was a huge disappointment. Payrolls increased by a less-than-impressive 266,000, following March’s downwardly revised 770,000 reading. With this, May’s figure will be widely watched. Note the three-month rolling average stands at 524,000, and the six-month rolling average falls in around 294,000.

According to the BLS[1], employment in leisure and hospitality increased more than 330,000 as a result of re-opening programmes across many parts of the country.

April’s figure weighed on the US dollar—as measured by the US dollar index (ticker: DXY)—though only a mild reaction was observed in US equities, through the S&P 500. This was largely due to the expectation the United States Federal Reserve is likely to maintain near-zero interest rates.

Additional notes:

- Losses were observed in manufacturing employment (-18,000) after two consecutive months of gains in March and February.

- Retail trade employment also fell in April by 15,000, following a 33,000 print in March.

- Construction employment ended April unchanged, yet the survey highlighted employment in the industry is up by 917,000 over the year but remains 196,000 below its February 2020 level.

The general consensus for May’s US non-farm payrolls is an increase in the range of 650,000.

(Source: Reuters)

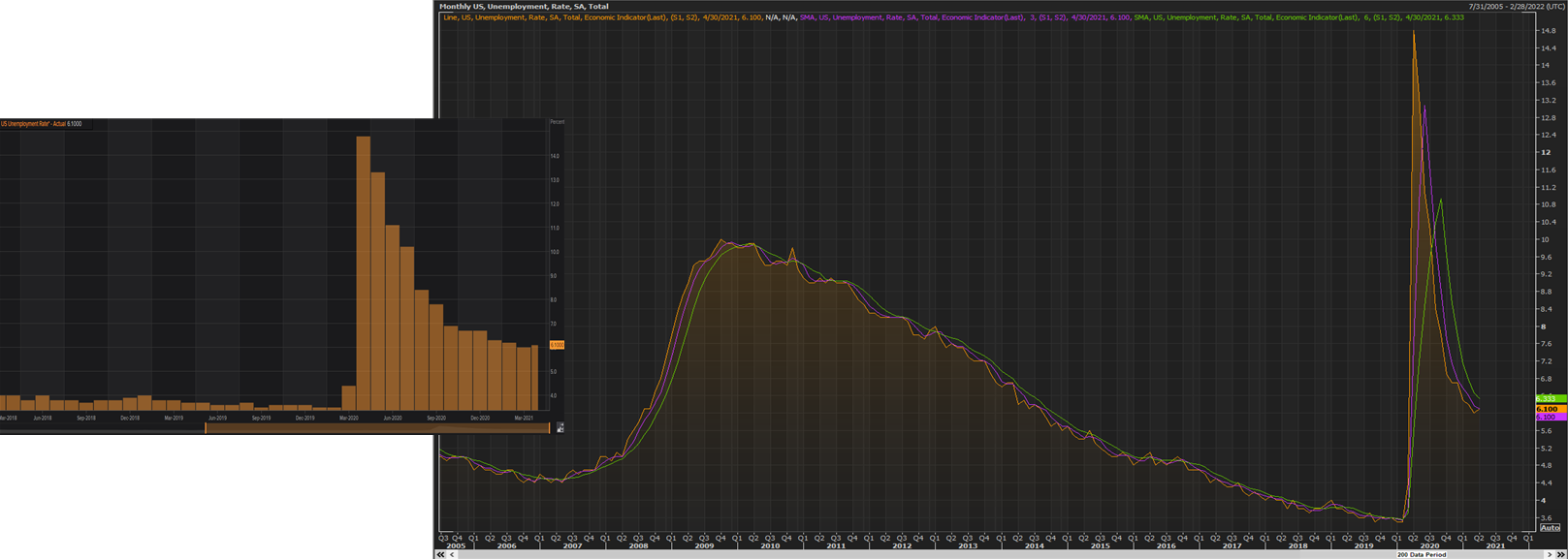

The Household Survey revealed unemployment was little changed in April, holding at 6.1 percent (March: 6.0 percent). Note the report’s official unemployment rate calculates by dividing the number of unemployed Americans (actively seeking employment) by the civilian labour force count.

Actively seeking is defined as those who applied for work in the past four weeks. Americans not seeking employment during the preceding four weeks are no longer counted in the civilian labour force, and are, therefore, included in the civilian noninstitutional population (figure found at the top of the household survey table).

According to the BLS, and also evident from the graph plotted below, April’s measures are significantly lower than April’s (2020) pandemic highs of 14.8 percent, but at the same time higher than pre-pandemic levels of 3.5 percent.

The real unemployment rate (U-6)[2]—a broader view of unemployment than the official (U-3) release—represents the total of unemployed in the United States, including all persons marginally attached to the labour force and total employed part time for economic reasons (The BLS notes that marginally attached are those who currently are neither working nor looking for work but indicate that they want and are available for a job and have looked for work sometime in the past 12 months. Discouraged workers, a subset of the marginally attached, have given a job-market related reason for not currently looking for work. Persons employed part time for economic reasons are those who want and are available for full-time work but have had to settle for a part-time schedule). As you can see, the official release is artificially depressed.

April’s U-6 unemployment figure came in at 10.4 percent, down 0.3 percentage points from March‘s 10.7 percent reading—the lowest reading since March 2020. It is also worth noting that April’s 2020 pandemic high came in at an eye-popping 22.9 percent, while the U-3 official release was, as noted above, 14.8 percent.

May’s official US headline unemployment reading is forecasted to tick lower at 5.9 percent.

(Source: Reuters)

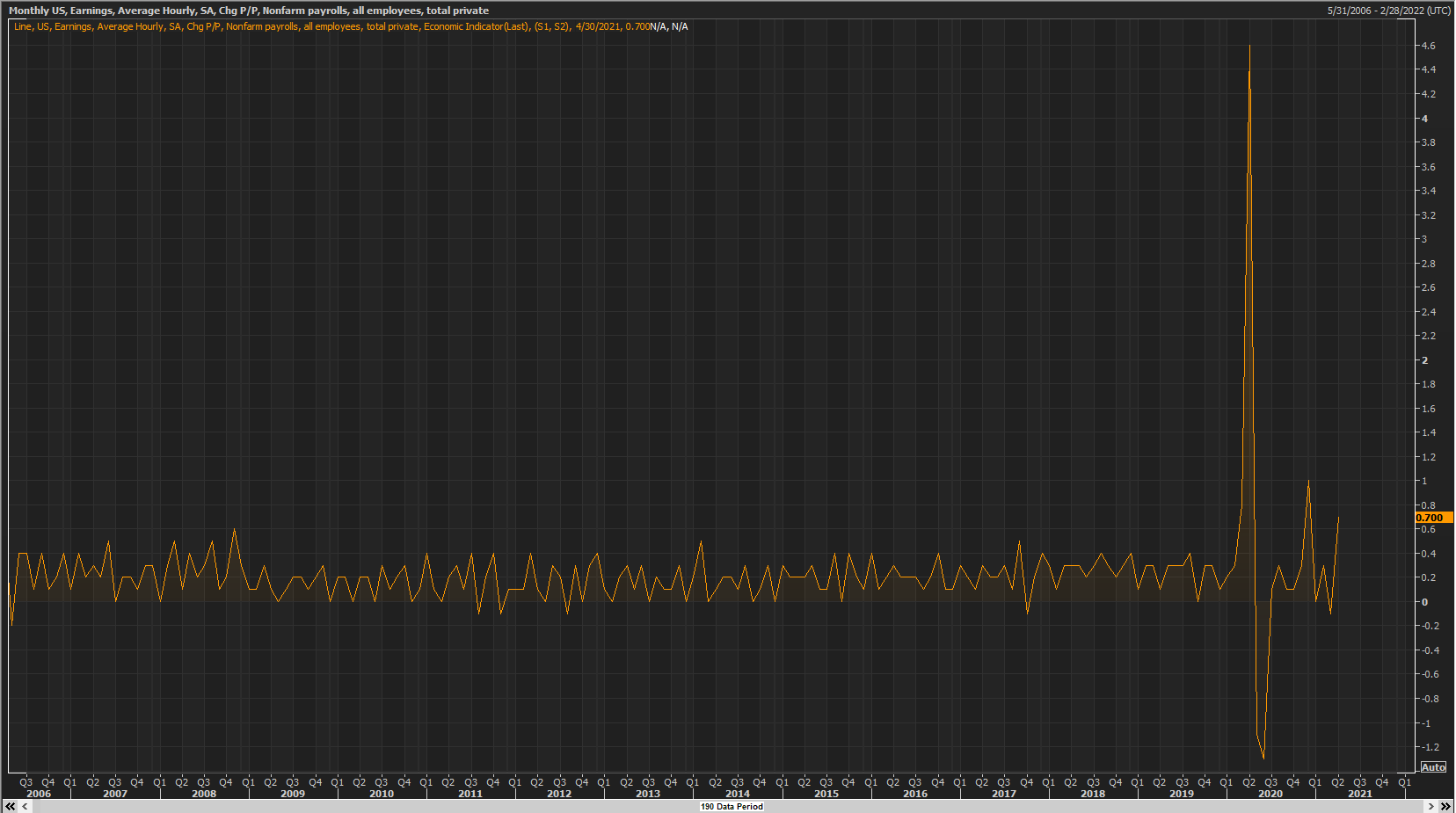

Calculated by the Establishment Survey, average hourly earnings is another key metric watched by economists and investors, measuring the amount private employees earn each hour in the United States.

In April, average hourly earnings suggested rising demand for labour, increasing by 0.7 percent from March’s -0.1 percent reading—this is the highest percentage print this year. (average hourly earnings for all employees on private nonfarm payrolls increased by 21 cents to $30.17, following a decline of 4 cents in the prior month—a touch higher than April’s 2020 reading of $30.07).

The importance of this measure is relatively self-explanatory. The more income a worker earns bodes well for future spending. It is an important indicator of labour cost inflation—one of the data points the United States Federal Reserve pays close attention to when formulating interest rate decisions.

The consensus for May’s average hourly earnings is forecasted to decline 0.2 percent.

(Source: Reuters)

FP Markets Technical View

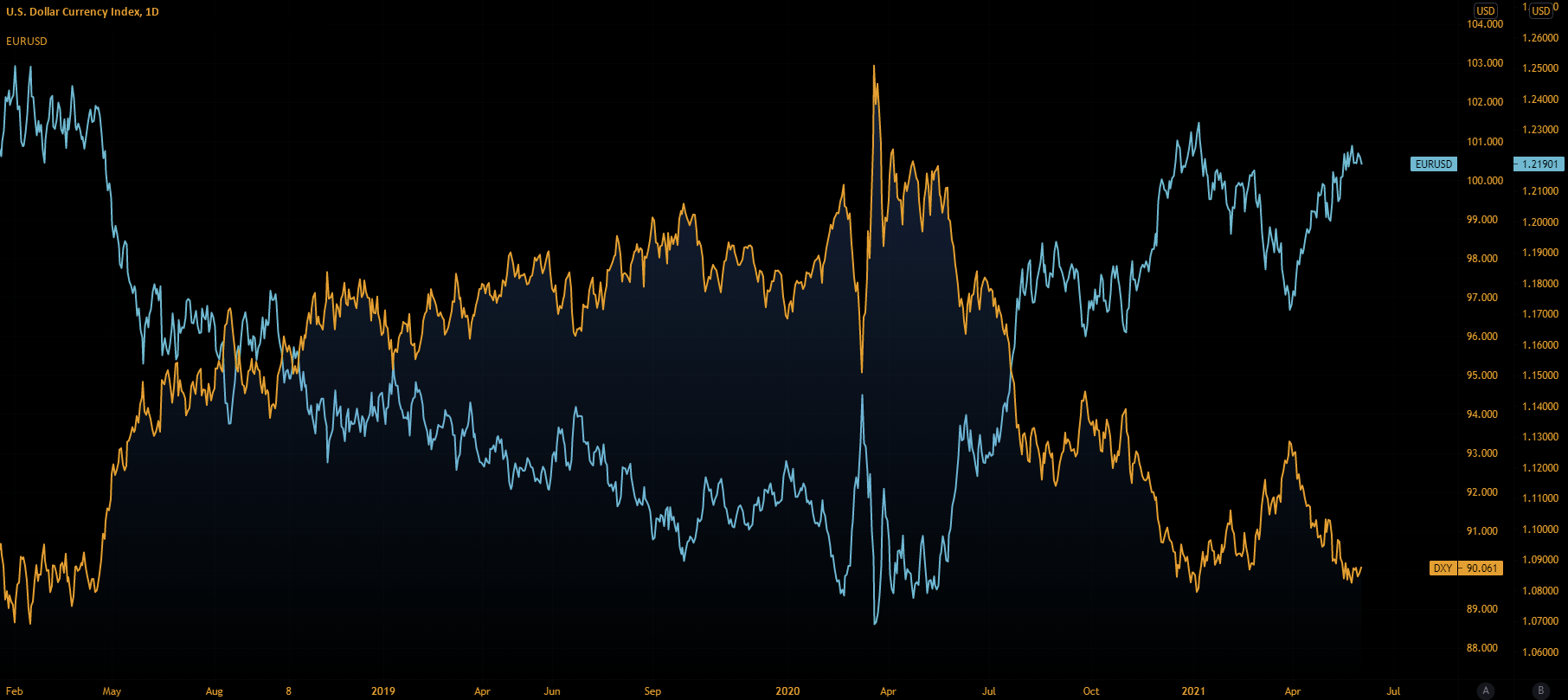

the US dollar index (ticker: DXY) provides traders and investors a benchmark value—a weighted geometric mean—of the US dollar relative to a basket of six major foreign currencies, including the euro (boasts the largest weighting of approximately 57.6%), Japanese yen, British pound, Canadian dollar, Swedish Krone and Swiss franc. Knowing Europe’s single currency plays a large role in the makeup of the DXY, it’s important to acknowledge the EUR/USD and DXY tend to be inversely correlated, as displayed in figure 1.A.

(Figure 1.A: EUR/USD Vs. US Dollar Index)

To gather an overall picture of the US dollar’s position ahead of today’s US employment release, the research team has analysed—from a technical perspective—the US dollar index according to the long-term monthly timeframe, the daily timeframe, as well as the H1 timeframe.

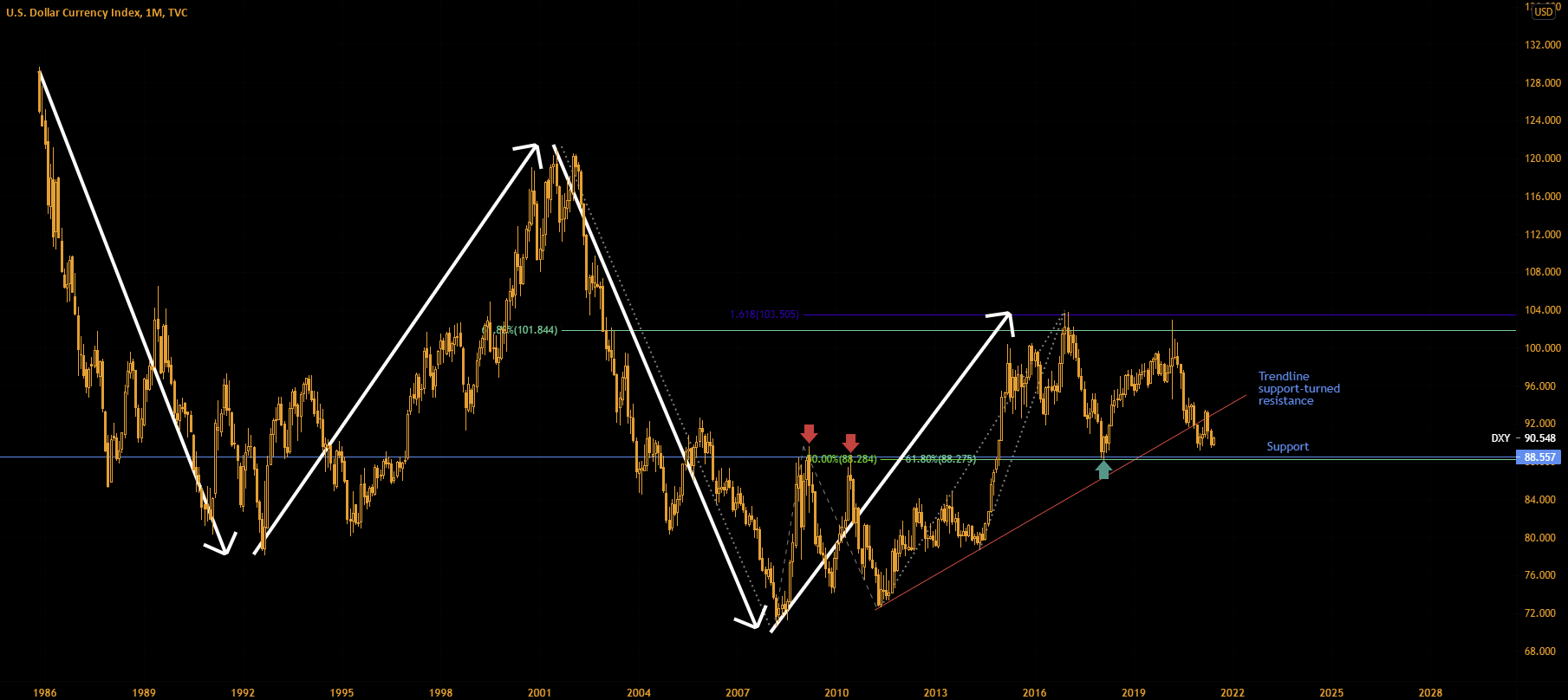

Monthly timeframe:

From the monthly chart, technicians will note April spun lower from a trendline support-turned resistance, extended from the low 72.69, with May extending downside to within striking distance of support from 88.55 (note we also have a 50% retracement level nearby at 88.28 and a 61.8% Fib at 88.27).

Overall, the major trend is lower (see arrows). Couple this with the recent trendline support breach, this emphasises a bearish USD market, long term.

(Source: Trading View—US dollar index monthly chart)

Daily timeframe:

A closer reading of price action on the daily scale shows we recently breached the upper side of what’s known as a declining wedge pattern (91.43/90.42). This—given the bearish narrative since March 31st peaks at 93.43—is likely considered a reversal signal, with buyers taking aim at 90.91 (the wedge pattern’s take-profit target, derived from taking the base measure and extending this value from the breakout point [red]).

As for trend on this timeframe, we can, in line with monthly price action, see this market has been entrenched within a downtrend since topping in early March 2020, just south of the 103.00 figure.

Also notable on the daily chart is we’re coming from support at 89.67 and, in recent days, elbowed north of resistance coming in at 90.10 (now labelled support).

Ultimately, traders are likely expecting a bearish reaction off 90.91, as sellers look to fade into the current pullback.

(Source: Trading View—US dollar index daily chart)

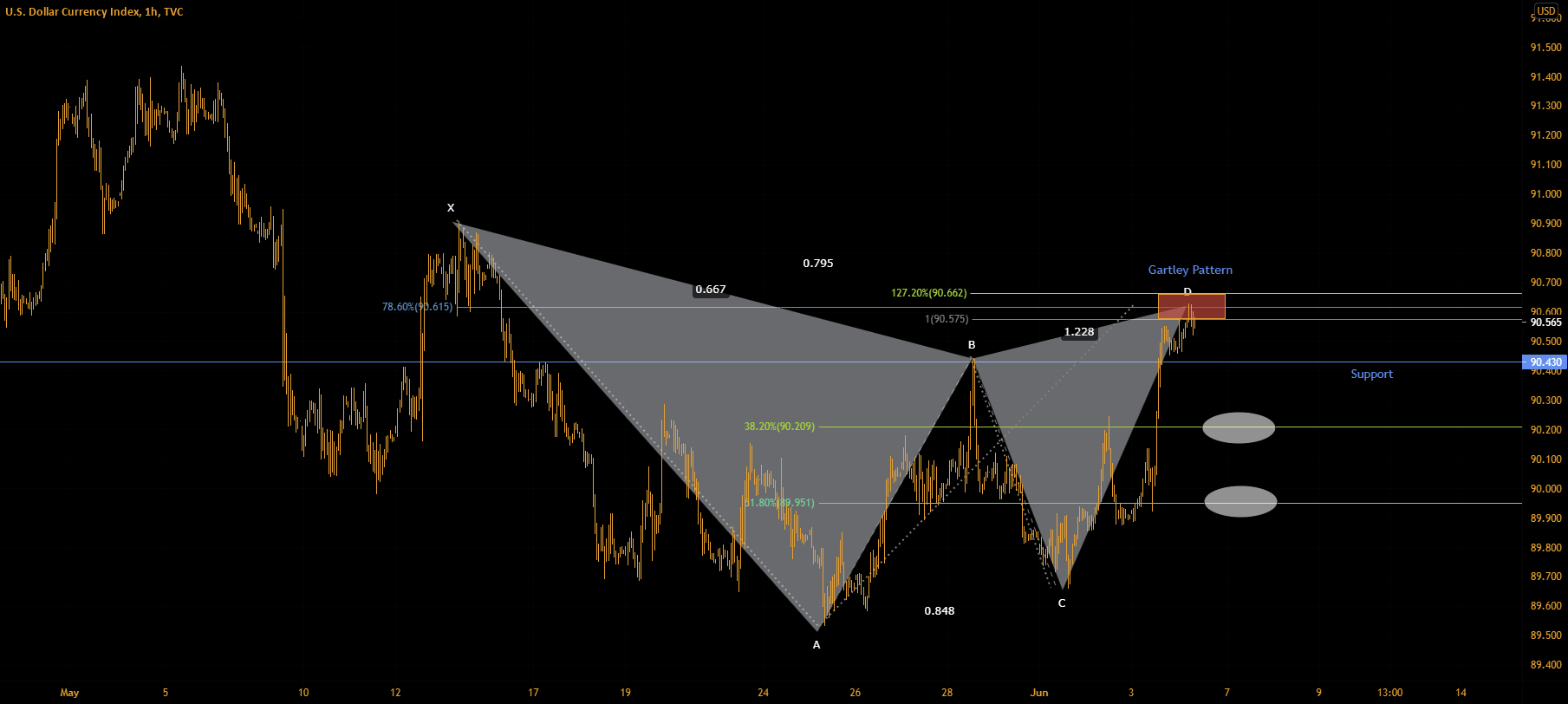

H1 timeframe:

From a shorter-term perspective, chart studies reveal the DXY recently touched gloves with a harmonic Gartley pattern (potential reversal zone [red] made up of a 78.6% Fib at 90.61, a 100% Fib projection at 90.57 and a 1.272% Fib extension at 90.66).

Should the above formation hold, support is considered an initial roadblock at 90.43, followed by the 38.2% Fib at 90.20 and the 61.8% Fib at 89.95 (values derived from legs A-D of the Gartley).

(Source: Trading View—US dollar index hourly chart)

DISCLAIMER:

The information contained in this material is intended for general advice only. It does not take into account your investment objectives, financial situation or particular needs. FP Markets has made every effort to ensure the accuracy of the information as at the date of publication. FP Markets does not give any warranty or representation as to the material. Examples included in this material are for illustrative purposes only. To the extent permitted by law, FP Markets and its employees shall not be liable for any loss or damage arising in any way (including by way of negligence) from or in connection with any information provided in or omitted from this material. Features of the FP Markets products including applicable fees and charges are outlined in the Product Disclosure Statements available from FP Markets website, www.fpmarkets.com and should be considered before deciding to deal in those products. Derivatives carry a high level of risk; losses can exceed your initial payment. FP Markets recommends that you seek independent advice. First Prudential Markets Pty Ltd trading as FP Markets ABN 16 112 600 281, Australian Financial Services License Number 286354.

Access +10,000 financial

instruments

Access +10,000 financial

instruments