Reading time: 15 minutes

Bias is defined as preference or inclination to favour a viewpoint or outcome.

Behavioural finance helps shape the way investments and the decision-making process are interpreted. Although researchers in the field of psychology have coined several classifications, cognitive and emotional biases form an umbrella for many common biases and are the focal point for this article.

Individual investors and traders are likely less susceptible to the effect of these biases if vigilant to the possibility of their occurrence.

Cognitive and Emotional Biases:

- Cognitive biases arise from information-processing or memory errors: ‘blind spots’.

- Emotional biases stem from impulse, influenced by emotions. According to traditional finance, diverging from rational decision making is a direct result of emotional biases.

Biases derived from faulty information processing are often easier to identify (and correct) than emotional biases. However, further education and better information can help alleviate both types of biases.

Note that specific biases may share cognitive and emotional components.

Cognitive Biases:

Cognitive biases are classified into two groups:

Belief Perseverance Biases:

A tendency to maintain established beliefs despite new evidence.

Information-Processing Biases:

The practice behind how market participants process information.

Belief Perseverance Biases:

- Conservatism Bias:

Serving as a belief perseverance bias, ‘conservatism bias’ involves maintaining prior views (or forecasts) and dismissing a new piece of information. This leads to excess weight on initial beliefs.

An example would be a long (buy) position on the British pound against the US dollar (GBP/USD) based on the expectation of an imminent interest rate hike.

The issue is the Bank of England (BoE), despite many desks pricing in a rate hike, leaves the bank rate unchanged at its next policy meeting, signalling an indecisive tone regarding upcoming movement.

This guides sterling south. Falling victim to conservativism bias here may result in holding the long position longer than justified, ignoring fresh information (downside in GBP/USD).

Another implication of this type of bias, and many of the following biases, is under-diversification of a portfolio, which can increase overall portfolio volatility.

- Confirmation Bias:

Recognising things that validate a view (or belief) and undervaluing aspects that counter an opinion is called ‘confirmation bias’ or ‘selective perception’.

After making an initial trading or investment decision, confirmation bias highlights information supporting a viewpoint. The difficulty is when a market participant observes only confirmatory information and overlooks (or modifies) contradictory evidence.

A long position on Tesla (TSLA) where the investor considers only positive news releases is a good example. The consequence is investors who concentrate on positive aspects and shelve negative views can lead to an investor holding a position longer than justified, similar to the effects of conservatism bias.

- Representative Bias:

When patterns appear similar, people might draw conclusions based on the comparison. Ranking or grouping new knowledge based on prior experience describes ‘representative bias’ (classifying information into personalised categories).

Even if new information does not correspond to these tailored groups, many adopt a ‘best-fit’ approximation if the information provided ‘resembles’ past experiences.

Cryptocurrencies sharing similar characteristics to the Dot-Com bubble remains a subject of debate and offers a good example of representative bias. Those accepting this belief may formulate trading ideas based on the resemblance, and as a result, fail to conduct in-depth research.

- Illusion of Control Bias:

‘Illusion of control bias’ is identified as a belief in which traders or investors feel they have a measure of control over the outcome of an event.

Those maintaining a belief they have influence over a tradeable market can lead to overtrading and excessive risk exposure. Illusion of control may also give rise to a bias known as ‘overconfidence bias’.

An example is an employee of a company. Working within an organisation can have some employees hold large positions in the company’s stock on the belief they have some type of the influence. It’s clear most investors—working for the company or not—possess little control over the price valuation of a company’s stock price or other financial instruments.

- Hindsight Bias:

‘Hindsight bias’ is described as observing previous events as a predictable occurrence.

People often remember predictions of the future as more precise than they actually were. Because people do not have perfect memory, they reconstruct the gaps they prefer to believe.

An example of this is overestimating the degree to which one predicted an outcome, consequently providing a false sense of confidence which may encourage a larger position size.

- Cognitive Dissonance Bias:

A state of imbalance emerges when newly acquired information creates a situation that conflicts with pre-existing interpretations or beliefs; this is a psychological phenomenon often referred to as ‘cognitive dissonance’.

Cognitive dissonance, along with other common behavioural biases such as confirmation and representative bias, is frequently experienced at market tops (and bottoms), particularly amidst early reversal phases. Traders and investors regularly hone in on market information confirming an upside bias, rather than acknowledging signals suggesting a market turn.

This behaviour at market tops, action refusing to include conflicting information, convinces traders and investors to hold positions longer than necessary. Overlooking a long-term trendline support breach or defensive stocks (staples, services and utilities, for example) demonstrating signs of upside is a sign of cognitive dissonance.

Information-Processing Biases:

- Mental Accounting Bias:

Mentally compartmentalising money is an information-processing occurrence known as ‘mental accounting bias’, in which people consider an equal sum of money differently over another.

While many acknowledge money is fungible (can be replaced by another identical object), the vast majority catalogue funds into mental baskets depending on its source and intended use.

A clear example of this is an investor overlooking capital depreciation for yield.

- Outcome Bias:

‘Outcome bias’ is common amongst newer investors.

It is an inclination to process information in an illogical manner, an approach in which decisions are made based on the outcome of previous events. The primary issue with this bias is while the outcome of previous events may have been a series of yearly positive returns, the process by which the positive returns were generated can be overlooked.

In simple terms, outcome bias underscores the outcome of an event and gives little weight to occurrences that led to the outcome.

What this can do is have investors invest in a strategy beyond their risk tolerance, as they hone in on the returns (past performance or outcome).

- Recency Bias:

To more prominently recall recent events more than events that occurred in the past is known as ‘recency bias’.

Most traders and investors fall victim to recency bias at one point or another in their careers: those who base their decision process on recent market movement rather than taking into account the overall market picture.

Although a number of problems can arise due to recency bias, the more obvious might be the case when a trader or investor places undue emphasis on recent price action and overlooks previous market data. An example might be the primary trend exhibiting a retracement. While the primary trend remains north, the retracement—or secondary trend—is down and, therefore, could have market participants process the short-term information as a downtrend and prompt a bearish approach, rather than seeking dip-buying themes in line with the primary trend.

Another instance may see market participants place emphasis on the asset class in favour due to the effect of recency bias.

Emotional Biases (Psychological Biases):

- Loss-Aversion Bias:

An emotionally-charged bias known as ‘loss aversion’ was developed by Daniel Kahneman and Amos Tversky in 1979 while developing ‘prospect theory’.

The paper states:

A salient characteristic of attitudes to changes in welfare is that losses loom larger than gains. The aggravation that one experiences in losing a sum of money appear to be greater than the pleasure associated with gaining the same amount (Kahneman & Tversky, 1979, Page 279).

Rational investing or trading, however, should accept more risk to increase gain, as opposed to accepting additional risk in an attempt to circumvent loss. Financial market participants, as a result, may hold positions longer than justified by their technical or fundamental approach (disposition effect).

Those influenced by loss aversion may also sell winning positions earlier than warranted through fear of the position eroding unrealised gain.

- Overconfidence Bias:

As its name implies, ‘overconfidence bias’ is traders and investors displaying unjustified faith in their subjective reasoning and abilities. It is often linked closely with the belief perseverance bias: illusion of control (see above). Consequently, overconfidence bias houses cognitive and emotional errors yet is classified as an emotional influence due to a larger proportion of emotional effects.

Like many emotional biases, overconfidence is difficult to correct. While confidence is imperative in trading and investing, as well as in other life endeavours, overconfidence can be detrimental. This might result in overestimating the expected return of a trade or investment, and, as many biases noted, encourage excessive risk-taking and under-diversification.

- Regret-Aversion Bias

Seeking to avoid the emotional discomfort of regret related to decision making is known as ‘regret-aversion bias’.

Regret, for many rational individuals, triggers emotional grief; in this case, the brain attempts to evade making decisions that cause regret.

Many traders and investors understand in order to generate consistent returns, not only must they have control over their approach—well-defined investment strategies—they must also maintain control over their psychological approach.

Regret aversion can result in market participants being too conservative, giving rise to underperformance. It can also open up what’s known as ‘herd behaviour’, as those experiencing regret aversion may feel somewhat ‘sheltered’ if many have a similar view.

Trader and Investor Psychology: Basic Interpretation

It’s a well-known truth that the market is driven by expectations of future prices, guided by beliefs, attitudes, habits and emotions. Group pressure can also influence decisions.

The final decision we make as traders and investors should, under usual circumstances, be guided by rational decision making. Reality is often different and the majority of decisions include psychological pressures.

Positive feedback loops are important to understand, which, although is a self-promoting movement, is unsustainable. A market top, for example, could begin by attracting attention due to a stock (or stock market) or currency pair being undervalued. This can form a bottom and show signs of strength—think trendline resistance breach—and result in additional investment flow. As price rises, this process repeats itself until it spirals out of control and forms a phase of irrational behaviour. This is a point where overconfidence bias can show itself. Once liquidity thins and prices begin displaying signs of weakness, a number of noted biases can arise cognitive dissonance and representative bias, for example.

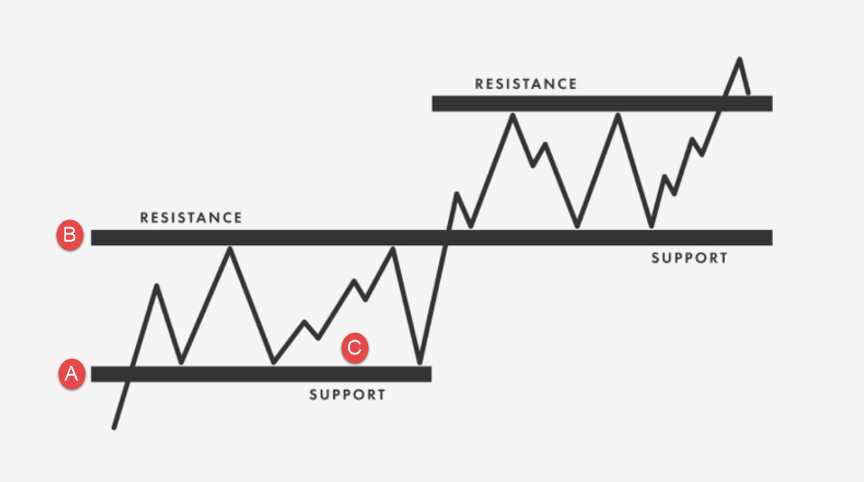

Market Trend Structure: Behavioural Tendencies:

While several explanations exist for trend-based price movement, below is one scenario explaining the potential behavioural psychology behind trend movements.

Figure 1A assumes a trend has just begun.

Price breaking through initial resistance at point A is likely to have attracted breakout buying, with the expectation of continuation moving higher. It is important to recognise that some traders long prior to the test of point A would have liquidated at the resistance.

However, at point B, we see upside momentum diminish which could be a result of loss aversion bias. This suggests breakout buyers may have been fearful breakout gains would erode and, therefore, liquidate positions for a small profit. This, alongside resistance drawn from history, caused a ceiling to form at point B.

The retest at point C (previous resistance at point A) is a common occurrence in financial markets and can often witness C develop support (referred to as resistance-turned support). Together with learned techniques, such as enter long a retest of a resistance-turned-support, and what’s known as a ‘regret bias’ (regret derived from traders and investors who liquidated positions at point A and thus re-entered at C), support forms at point C.

As the trend persists, similar occurrences unfold. Hindsight bias can help explain why trends persist as traders and investors look to previous events and believe (overestimate) their ability to time the dips to enter long. This is also linked closely to the illusion of control and overconfidence bias. As the trend starts to show strength, confidence builds and market participants believe they have some control over the outcome of the event.

What can also fuel trend strength is representative bias. A prolonged move has traders and investors devise trading ideas on the similarity of previous events, or in this case, trends, and consequently fail to do the required research. Other biases also contribute to a trend’s formation, such as confirmation bias and cognitive dissonance bias.

The Reality of Trading and Investing

Recognising and understanding common behavioural tendencies is recommended for learning. The ability to trade and invest successfully requires in-depth knowledge not only of the markets but also of one’s psychological mindset. By educating oneself on the biases and their effects help make one less susceptible to their effect and can ultimately benefit your investment decision-making and investment performance.

Human behaviour, or investor behaviour, is an exciting field of study, with many additional biases to consider that affect financial decisions, such as ‘anchoring bias’, ‘familiarity bias’, ‘status quo bias’ and ‘self-attribution bias’. If further study is required, consider watching our webinar here.

Access +10,000 financial

instruments

Access +10,000 financial

instruments